Higher Education: The Next Financial Crisis?

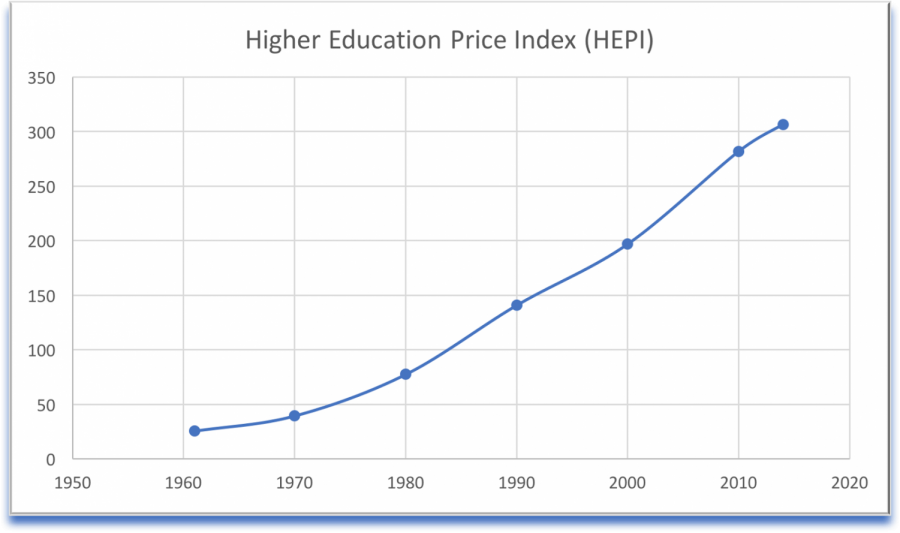

A graph showing the inflation rate of higher education as recorded by the Commonfund Institute HEPI model.

January 11, 2018

Are you a high school student preparing to graduate within the next four years? Are you planning to attend a two or four year college and get a degree before entering the workforce?

If so, you might be shocked to discover that there may be an economic bubble in higher education- and it could be getting ready to burst.

In order to predict the future, one must first study the past. The most notable financial bubble to burst in recent memory is that of the real estate market. The crash of the real estate market in the late 2000’s led to the so-called ‘Great Recession’ in the ensuing years.

In early 2007, the U.S. real estate bubble popped, with dozens of real estate mortgage lenders and banks filing for bankruptcy or claiming massive financial losses. As many as 10 million Americans lost their homes to foreclosure as a result of the 2007-2009 financial crisis, according to the National Policy Center[1].

The causes of the real estate crash are still debated, but several key events are agreed upon as detrimental to the integrity of the system as a whole.

The simplified version of history that most economists agree with went like this:

Sometime during the late 20th century, someone decided the housing market needed to be expanded. Banks handed out loans to people who could not afford them (subprime loans). Then these banks manipulated the loans to make them appear more legitimate to creditors and ratings agencies. This gave the appearance of legitimacy to loans that would usually be considered high-risk (because the people could not pay back their loans).

The result of this is that investors in the domestic and global markets could not see that the loans were no good, causing speculative investments (a term which describes investments where there is a substantial risk of losing all assets).

Then, these people with bad credit backed out of the loans because they could not afford to pay for them. Everyone who had put money into the loans, the investors, as well as regulatory agencies paid the price in the subsequent collapse.

The taxpayers then fund these defaulted loans, through legislation such as the The Mortgage Forgiveness Debt Relief Act of 2007. This act “generally allows taxpayers to exclude income from the discharge of debt on their principal residence”, according to the IRS[2].

The banks lose business (e.g. Lehman Brothers closing), people lose their homes, and investors and taxpayers lose their money.

Now, the nuances of the crisis are still unclear. Economists Stephen Horowitz and Peter Boettke blame the Federal Reserve’s excessive interest rate cutting in part for disturbing the market[3].

Public policy analyst Randal O’Toole concluded in his book American Nightmare: How Government Undermines the Dream of Home Ownership that government involvement in the housing market crash was brought upon primarily by a conflict between state and local laws restricting supply and federal laws attempting to artificially increase demand[4].

Economists such as Paul Krugman[5] reject this line of reasoning. He stated that the specific anti-discrimination laws that some free market enthusiasts villify have had little effect on the failure of the housing market.

Generally, the consensus among economists[6][7][8] is that the expansion of credit and the increasingly bad loans that people did not pay back were some of the main causes of the crash.

Sound familiar? It should, because that is exactly the situation that the United States higher education market is in right now.

To understand the college bubble, you have to understand the boundaries between government and business in a free market system. Government cannot assume the roles of businesses in a free market; nor can business assume the role of government.

The law of supply and demand is the key. This fundamental principle of economics states that supply and demand have an inverse proportional relationship (as one increases, the other decreases). Of course, this is a vastly simplified version of the law as there are various other factors that affect both supply and demand. But, for the sake of clarity and transparency, we need only discuss the main points.

Now, this is an example of government interference in supply and demand. There was already a certain level of demand in he housing market. Apparently, the government wanted to artificially expand the market (and big banks were all too happy to oblige). The only way that this could be accomplished was to have government back up the losses that resulted from lending to bad creditors.

The events followed a succession like this:

Step one: the market is not large enough; alternatively, the market does not cover enough of the population.

Step two: expand the market by giving people loans to pay back their debt[9].

Step three: the government covers any risk associated through these risky ventures with federal money to agencies are huge bailouts[9].

Step four: people don’t pay their loans.

Step five: so-called ‘debt forgiveness’ forces taxpayers to pay the price of loan defaults[9].

Step six: POP.

In the market of higher education, prospective students are given large loans to buy an asset that they believe will allow them to pay it back. People assume an increasingly large amount of debt that they probably will never work off.

The price of college has skyrocketed, as private education costs rose 1,000%. The price of all commodities rose 280% and housing rose about 400%[9].

The federal government has already assumed the risks of these loans through the establishment of Sallie Mae to encourage more bank loaning, Stafford and Perkins loans (FAFSA), the Affordable Care Act’s direct student loans, and various other public programs.

And what happens when a mass amount of people don’t pay these loans?

It’s almost poetic.

Professor Anthony Davies of Duquesne University explains:

“Just as the government sought to engineer people into houses, it now seeks to engineer them into higher education…. By law, lenders cannot even deny Stafford and Perkins loans (types of federal student loans) based on the borrower’s credit or employment status. What other reason is there to deny a loan?

“And just as home buyers took out loans to speculate on houses they could never hope to afford, students are taking out loans to cover educations they often cannot complete and which often do not hold value in the market even when completed. Government meddling has again separated profit from risk. Universities get to keep the tuition profits while taxpayers are forced to shoulder the risk of students not paying back their loans. Once again government has created the conditions for wholesale failure, and failure is upon us.”[9]

It’s not as if the causes of the bubble are top-secret information; even the Federal Reserve linked government loans to artificially sky-high tuition prices. In a July 2015 study (revised in 2017), three economists writing for the Federal Reserve Bank of NY found “a pass-through effect on tuition of changes in subsidized loan maximums of about 60 cents on the dollar, and smaller but positive effects for unsubsidized federal loans.”[10]

In a field like economics, it is often difficult to accurately predict trends and business cycles because of the volatility of the market and a severe lack of information.

No one can predict with absolute certainty the future of any market, including that of higher education. Accordingly, it is important to note that not all economists agree that the higher education market is in for a crash.

Some, like Joseph Hogue, a former economist for the state of Iowa, believe that there is a crisis in student debt but it cannot be characterized as a bubble because it is not ready for a sudden pop or crash[11].

Others disagree that the ‘bubble’ is an imminent danger at all[12].

There is, however, a consensus among experts that such a bubble exists[13][14][15][16].

In the coming years, prospective college students ought to be weary when entering the higher education market- they might be caught in the middle of a crash.

Sources:

http://www.nber.org/digest/may13/w18609.html

[1]“The 2008 Housing Crisis Displaced More Americans than the 1930s Dust Bowl.” National Center for Policy Analysis, www.ncpa.org/sub/dpd/index.php?Article_ID=25643.

[2]https://www.irs.gov/newsroom/home-foreclosure-and-debt-cancellation

[3]Boettke, Peter J., and Stephen Hororwitz. “The House That Uncle Sam Built | Peter J. Boettke.” FEE, Foundation for Economic Education, 5 Jan. 2016, fee.org/resources/the-house-that-uncle-sam-built/.

[4]OToole, Randal. American nightmare how government undermines the dream of home ownership. Cato Institute, 2012.

[5]https://krugman.blogs.nytimes.com/2009/11/10/armey-of-ignorance/

[6]Wallison, Peter J. Hidden in plain sight: what really caused the world’s worst financial crisis and why it could happen again. Encounter Books, 2016.

[7]Duca, John V. (Federal Reserve Bank of Dallas) (2014). “Subprime Mortgage Crisis”. Federal Reserve History. Federal Reserve. Retrieved May 15, 2017. “The expansion of mortgages to high-risk borrowers, coupled with rising house prices, contributed to a period of turmoil in financial markets that lasted from 2007 to 2010.”

[8]“Missteps to Mayhem.” Vanderbilt University, news.vanderbilt.edu/vanderbiltmagazine/missteps-to-mayhem/.

[9]Davies, Anthony. Why the Education Bubble Will Be Worse Than The Housing Bubble. 2012. https://www.usnews.com/opinion/blogs/economic-intelligence/2012/06/12/the-government-shouldnt-subsidize-higher-education

[10]Lucca, David o, et al. Credit Supply and the Rise in College Tuition: Evidence from the Expansion in Federal Student Aid Programs. 2015, Credit Supply and the Rise in College Tuition: Evidence from the Expansion in Federal Student Aid Programs.

[11]Marquit, Miranda. “Is the Student Loan Bubble Ready to Pop? One Expert Weighs In.” Student Loan Hero, 27 June 2017, studentloanhero.com/featured/student-loan-bubble-whats-next/.

[12]Harris, Malcolm. “There is no college bubble”. Web. https://www.theawl.com/2015/10/there-is-no-college-bubble/

[13]Burns, Scott. “The College Bubble and the Austrian Business Cycle | Scott Burns.” FEE, Foundation for Economic Education, 31 Dec. 2015, fee.org/articles/the-college-bubble-and-the-austrian-business-cycle/.

[14]Rogers, Jim, and Robert Craig Baum. “This Economic Bubble Is Going to Wreak Havoc When It Bursts.” Fortune, 10 July 2017, fortune.com/2017/07/10/higher-education-student-loans-economic-bubble-federal/.

[15]Thompson, Derek. “This Is the Way the College ‘Bubble’ Ends.” The Atlantic, Atlantic Media Company, 26 July 2017, www.theatlantic.com/business/archive/2017/07/college-bubble-ends/534915/.

[16]Foroohar, Rana. “The US college debt bubble is becoming dangerous.” Financial Times, 9 Apr. 2017, www.ft.com/content/a272ee4c-1b83-11e7-bcac-6d03d067f81f.